On Jan. 7, the Consumer Financial Protection Bureau issued a new rule prohibiting consumer reporting agencies from including medical debt on credit reports. However, on Jan. 20, President Donald Trump issued an executive order halting new rules by the agency.

In Olympia, state Sen. Marcus Riccelli, D-Spokane, is sponsoring Senate Bill 5480 to exempt medical debt from Washingtonians' credit reports and to prohibit providers from reporting medical debt to consumer reporting agencies. The bill has passed the Senate (35-12, with two members excused), and the majority of the House Committee on Consumer Protection and Business gave the bill a "do pass" recommendation. The bill is expected to be scheduled for a House floor vote soon, and if passed, will head to Gov. Bob Ferguson's desk for his signature.

Ferguson hasn't indicated if he would sign the bill into law, but as Washington's Attorney General he championed cases targeting medical debt collectors, providing $157.8 million in refunds and debt forgiveness over unlawful medical charges to Washingtonians who likely qualified for free or reduced-cost hospital care.

In June 2024, Fair Health Prices Washington, a partnership of patient groups, nonprofit consumer advocacy organizations and labor unions, conducted a 1,000-person survey online in Washington. All participants were registered to vote in Washington and the results were statistically weighted to ensure the survey's sample reflected state demographics.

Some of the findings highlighted drastic issues with medical debt.

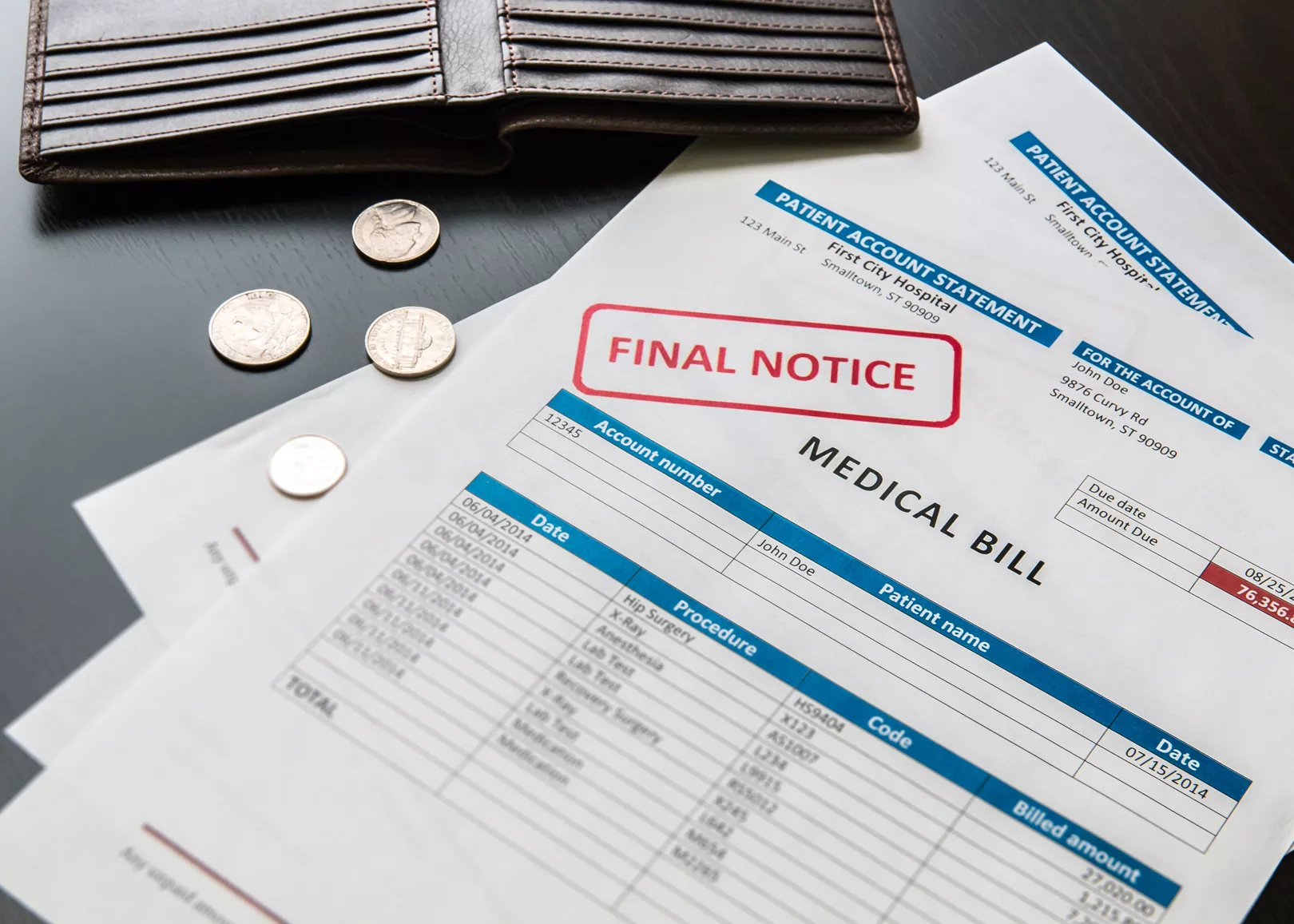

When asked, 31% of survey respondents said their households had unpaid medical debt. More than half of all respondents (57%) said they avoided seeking medical treatment or modified their use of prescriptions in the last year due to cost. Additionally, 67% of respondents said they would struggle or could not afford to pay an unexpected $500 medical bill.

Riccelli says the bill strikes a chord with his constituents and people statewide, because everyone knows someone impacted by medical debt problems. He says a chronic illness or an emergency room visit could quickly add up to $40,000. Unpaid debt can have systemic effects on credit reports, making it harder to rent an apartment, buy a home or get a job.

"Twenty-nine percent of Washingtonians have a lower credit score because of medical debt, and almost one in four are contacted by a debt collector because of their medical debt," Riccelli says. "It's important to note that a lot of these folks are doing everything right, and they're paying their bills."

Adam Zarrin is the director of state government affairs for the Leukemia & Lymphoma Society, a nonprofit focused on curing blood cancers and a policy advocate for improving the quality of life for patients and their families.

Zarrin says blood cancer is one of the most expensive cancers to treat, and treating any type of acute leukemia can cost half a million dollars in the first year after diagnosis. He says the out-of-pocket costs for treating cancer can balloon quickly.

"We know that for cancer patients, when they face out-of-pocket costs like that, they have to make really difficult decisions on whether or not to start or delay their treatment," Zarrin says. "In fact, four in 10 cancer patients will delay treatment or stop treatment altogether because of cost, and that's even true for patients who have adequate insurance."

Many cancer patients set up GoFundMe accounts, liquidate savings and/or take out a second mortgage, but within two years, about 42% of cancer patients will spend all of their life savings, Zarrin says.

"Often, many are putting their medical bills on credit cards, or leaving it as medical debt, as money owed to a provider or a hospital because you want to save your life," Zarrin says. "Because you delay your treatment, or you cut pills in half, it starts taking this kind of emotional, mental toll on you because you feel trapped by your debt."

The bill in Olympia goes further than what the federal rule would have done, by prohibiting the confiscation of wheelchairs, ventilators, insulin pumps, cardiac monitors, prosthetics and many other devices by medical debt collectors.

"That doesn't happen very often — it's rare — but can you imagine somebody coming to repossess your prosthetic arm," Riccelli says. "That's another thing this bill does — it bans those egregious practices that I think we can all agree are particularly horrific."

The Leukemia and Lymphoma Society is seeing similar bills move through other state legislatures. California, Colorado, Illinois, Minnesota, New York, and seven other states already have laws restricting medical debt reporting.

Zarrin says that medical debt is not a choice someone has made and often involves billing errors that insurance could have covered.

"I think there's a movement and an understanding that medical debt is unlike all other types of debt and shouldn't limit your ability to get lines of credit," Zarrin says. "You don't choose to get cancer, you don't apply to have leukemia, that's a very key difference versus a student, car or home loan."

Riccelli doesn't believe medical debt is a reliable predictor of someone's ability to repay other loans. He similarly says medical debt is often prone to billing errors, and credit reports shouldn't punish people who accumulate debt for reasons out of their control.

"We all could be one bad health emergency away from a fiscal burden that would be overwhelming," Riccelli says. "And I struggle with the notion that just because you have cancer, you are not allowed to try to get housing or try to get a job." ♦